As customers, longstanding and new, the way we interact with banks and manage our personal spending, borrowing and saving is experiencing drastic change. New digital offerings in the form of apps and online banking show commitment to customer centricity, but overall, banks are slow to adapt to the pace of change. The vast majority of bankers do recognize the strategic need to respond to their industry’s digital disruption, and are busy assessing and developing transformative technologies such as mobile, blockchain and artificial intelligence, trying to find an emerging market need and a robust business model.

How Should Banks Adapt?

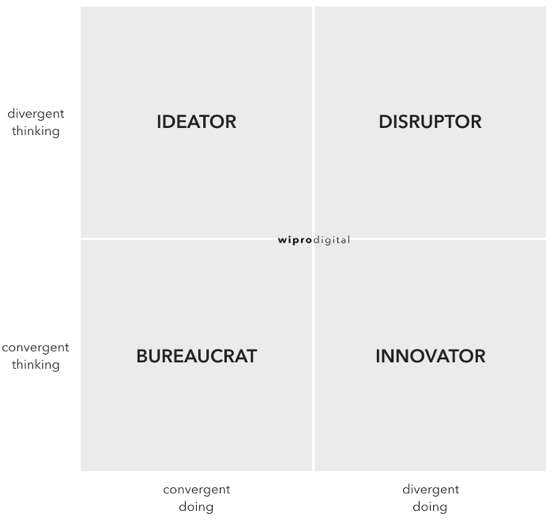

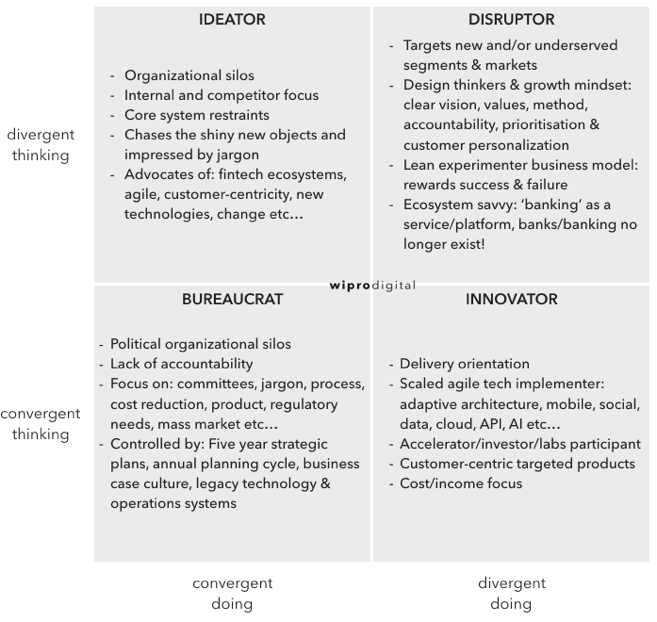

The operating environment of banks is unpredictable and, therefore, requires organizational agility. This agility requires a careful analysis of customer needs and (potential) capabilities. Bankers must ask, “How can my bank move from convergent thinking to divergent doing?”

From a strategic perspective, it’s essential to understand whether the person/organization wants to be a disruptor, innovator, ideator or bureaucrat. This differentiation defines the right strategic options available to them.

N.B.: A quick proxy answer to the above question is the design of the bank’s reception and organization of the people working there, to see if it is like every other bank, or is in some way distinctive.

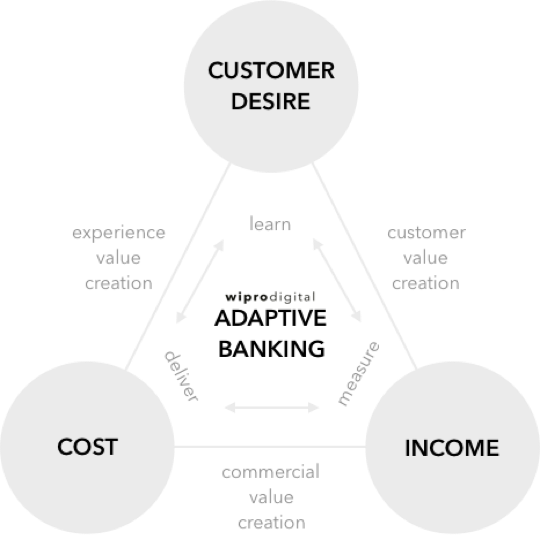

Value Triangulation and Differentiation

Every banking CEO needs a clear strategy that addresses their organization’s internal and external challenges. There is one global commonality for a strategic foundation: Every bank needs to deliver change rapidly and frequently. The better a bank is at improving customer experience, the more likely it will survive the onslaught of disruptors and innovators. Additionally, most banks must deliver cost reduction and drive income. Customer desire, the third corner of the triangle, is not a familiar banking concept, but a successful value triangulation delivers customer desire in the most efficient way possible.

This isn’t about value chain mapping and cost re-engineering; it’s about creating great customer experiences with adaptive capabilities and capital-light business models. All three values must be understood and practiced throughout the entire organization, especially among boards, chief executives and key decision makers to make adaptive banking possible.

Customer Experience Comes First

A culture of centralization, product-centricity and control-via-process stifles change. To be adaptive and create their own Digital DNA, banks must form new work spaces and ways of working. When bank employees don’t use their own company’s products, they are out of touch with the customer experience. They also may excuse customer complaints based on their organizational knowledge. Employees need to be the bank’s most critical customers, and ought to feel fully connected to other customers and their experiences.

New, lean business models should flow through the organization and align to the desired customer experience. The business leaders who identify the “priority customer experience features” will focus the organization on accelerating delivery momentum. Rather than requesting large-scale, product-led programs, leaders need to focus on continually launching and redefining small-scale features.

Doing so moves away from the grand strategies or silver bullet approach so often prevalent during annual planning cycles and shifts toward agile, customer-centric strategies. Organizational change is fundamental for creating adaptive banks with Digital DNA.

Fail Fast, Succeed Even Faster

To accelerate growth, adaptive technology architectures and agile software delivery methods need to be available to deliver the relevant features. A “deliver, measure and learn” approach will amplify feedback across the organization to drive commercial decision-making. This will allow banks to fail fast, yet succeed even faster. The ongoing cycle—ideating, designing, building, shipping, measuring, learning and (of course) adjusting customer features—needs to become the norm.

By becoming adaptive, the bank’s capabilities (people, methods, technologies, values) become more attuned to customer needs, making it far easier to deliver personalized offerings. For example, the bank’s data can be used to create feature personalization, allowing customers to pick and choose the right features for their needs. A customer should always be able to overwrite the choice an algorithm provides.

Innovation, Transformation and Beyond

Currently, the most apparent transformation desire and delivery exists in IT departments as opposed to business departments. Agile ways of working are often still alien to most bankers in product, finance, compliance, marketing and front-line teams.

The banking playbook has already been rewritten for the digital age. It’s an exciting time to realize great change and how disruption/innovation can become commercial reality—this means bucking the system.

About the Author / Darren Oddie

Darren Oddie is strategy director at Wipro Digital, where he works with global financial services companies on digital transformation and innovation. He’s had hands-on experience of designing and building financial services brands from a blank sheet of paper to industry leading propositions in both corporates and startups. He’s delighted that banking and customer experience are now regularly mentioned in the same sentence. Connect with him on Twitter.